A Significant Deficiency in Internal Controls Is Best Described as

Which best describes Jeffersons communication requirements. To be considered significant the deficiency must allow a misstatement that is more than inconsequential to be more than remotely likely to occur.

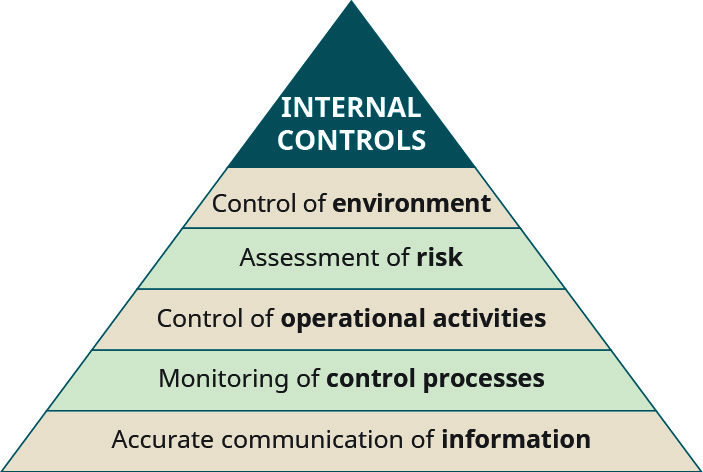

Define And Explain Internal Controls And Their Purpose Within An Organization Principles Of Accounting Volume 1 Financial Accounting

Two of these conditions are considered to be material weaknesses.

. Two of these conditions are considered to be material weaknesses. The auditor is required to communicate all deficiencies in internal control to management deficiencies that constitute a significant deficiency to the audit committee and deficiencies that constitute a material weakness to the full board of directors. The most effective internal control environments include both entity and activity level controls.

Stating that management has disclosed to the auditor all deficiencies in the design or operation of internal control over financial reporting identified as part of managements evaluation including separately disclosing to the auditor all such deficiencies that it believes to be significant deficiencies or material weaknesses in internal control over financial reporting. Finding the right internal control balance. A significant deficiency in internal controls is best described as a substantial weakness in internal controls that is less than material.

The determination of whether an account or disclosure is significant is based on inherent risk without regard to the effect of controlsA11 A significant deficiency is a deficiency or a combination of deficiencies in internal control over financial reporting that is less severe than a material weakness yet important enough to merit attention by those responsible for. The standards require that. In internal control is defined as a deficiency or combination of deficiencies that results in a reasonable possibility that a material misstatement would not be prevented or detected on a timely basis.

In internal control is defined as a deficiency or. This would encompass disclosing a change including an improvement to internal control over financial reporting that was not necessarily in response to an identified significant deficiency or material weakness ie. The implementation of a new information system if it materially affected the registrants internal control over financial reporting.

Any deficiencies in internal control that relates to compliance operation and non-financial reporting activities that adversely affects the likelihood that the entity will achieve its objectives. 527 What options are available to the auditor for presenting reports on the entitys financial statements and internal control over. By Howard B.

To determine the best balance and type of internal controls to implement NFPs need to assess several factors such as. Jefferson CPA has identified five significant deficiencies in internal control during the audit of Portico Industries a nonpublic company. Jefferson CPA has identified five significant deficiencies in internal control during the audit of Portico Industries a nonpublic company.

Paragraphs 22 through 23 of this standard discuss materiality in an audit of internal control over financial reporting and paragraphs 130 through 140 provide additional direction on evaluating deficiencies in internal control over financial reporting. A segregation of incompatible functions is necessary to ascertain that internal control is effective. The ability to segregate duties among accounting staff and management.

The auditor is required to communicate all deficiencies in internal control to management and deficiencies that constitute a significant deficiency or a material weakness to management and the audit committee. A weakness in the design or operation of a control. Which of the following best describes an auditors responsibility with respect to communicating internal control deficiencies of issuers.

D Written communication is required for material weaknesses but oral communication is allowed for significant deficiencies. A control deficiency or a combination of control deficiencies in internal control over financial reporting such that there is a reasonable possibility that a material misstatement of the companys annual or interim financial statements will not be prevented or detected on a timely basis b. Jefferson CPA has identified five significant deficiencies in internal control during the audit of Portico Industries a public company two of these conditions are considered to be material weaknesses.

On to define a significant deficiency and a material weakness respectively. A significant deficiency is a single weakness or a combination of weaknesses in the internal controls associated with financial reporting that is less severe than a material control weakness and yet is sufficient to merit the scrutiny of those responsible for administering an entitys financial reporting. Deficiencies in Internal Control over Operations Compliance and Reporting other than External Financial Reporting.

The CPA communicates all of the five significant deficiencies to management. Which best describes Jeffersons communication requirements. Which best describes Jeffersons communication requirements to the audit.

AThe auditor is required to communicate all deficiencies in internal control to management deficiencies that constitute a significant deficiency to the audit committee and deficiencies that constitute a material weakness to the full board of. A significant deficiency is a single weakness or a combination of weaknesses in the internal controls associated with financial reporting that is less severe than a material control weakness and yet is sufficient to merit the scrutiny of those responsible for administering an entitys financial reporting. Auditors are required to communicate to audit committees or others charged with governance significant control deficiencies including material weaknesses as these terms are defined in the applicable standards ie AU-C section 285 or for SEC issuers Auditing Standards AS 1305 and 2201.

A deficiency indesignexists when. 05A deficiency in internal control exists when the design or operation of a control does not allow management or employees in the normal course of performing their assigned functions to prevent or detect and correct misstate- ments on a timely basis. 14 When considering internal control an auditor should be aware of the concept of reasonable assurance which recognizes that the.

A significant deficiency is a control deficiency or a combination of control deficiencies that limits the ability to record process or report financial data in accordance with generally accepted accounting principles.

Nutrition Basics With Pdf School Nutrition Group Meals Health And Nutrition

10 Tips For Evaluating Internal Control Deficiencies Auditboard

What Are Internal Controls Types Examples Purpose Importance

No comments for "A Significant Deficiency in Internal Controls Is Best Described as"

Post a Comment